通过此次交易,道达尔能源还获得了路易斯安那州 Harvest Bend 项目 65% 的经营权益,以及德克萨斯州 Coastal Bend 项目 50% 的权益,但这家法国能源巨头计划在 Talos 收购完成后剥离这两项业务。

TotalEnergies 对 Bayou Bend 的兴趣与该项目靠近其 Port Arthur 炼油厂和 La Porte 石化设施有关,这将减少其在美国境内的排放。

今年 4 月,总部位于休斯顿的能源基础设施公司 Kinder Morgan 同意从 TGS Cedar Port Partners 租赁 10,800 英亩土地用于海上 CCS 开发,TGS Cedar Port Partners 是一家铁路服务运营商,负责管理休斯顿航道附近一个占地 15,000 英亩的工业园区。

WoodMac: CO2 Storage Demand To Outstrip Supply to 2034 Despite Explosion in New Projects

Government grants and tax incentives will drive carbon capture, storage, and/or utilization projects in the next decade as the industry seeks profitable business model.

The Northern Lights CCS site in Øygarden, Norway, operated by Equinor in joint venture with Shell and TotalEnergies.

Source: Kjersti Nordøy, Equinor

Over the next decade, global carbon capture, utilization, and storage projects (CCUS or CCS if without a utilization component) will require $196 billion in new investment to meet projected industrial demand in 2034, according to a market forecast Wood Mackenize released in late June.

By 2034, the world’s CCUS capacity will have grown to 440 mpta but with industrial demand reaching 640 mpta, only 66% of global needs will have been met, WoodMac reported.

Of projects already announced and expected to enter the development pipeline, 71% are in North America and in Europe, whose crown jewel and the world’s first cross-border facility for carbon injection and storage—the Northern Lights joint venture of Equinor, TotalEnergies, and Shell—expects to receive its first CO2 by ship from north Europe later this year.

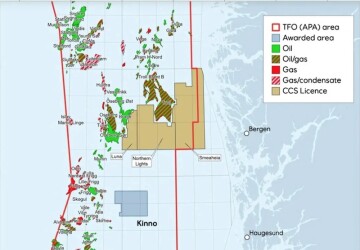

On 20 June, Norway’s Ministry of Energy named Equinor 100% owner and operator of two new North Sea CO2 storage licenses: Albondigas and Kinno, each with an estimated but unconfirmed storage capacity of 5 mtpa.

In 2022, Equinor won sole control of the Smeaheia license, a storage prospect adjacent to the Northern Lights storage license area and the route of a planned 25–35 mpta carbon export pipeline from Belgium and France, aptly named CO2 Highway Europe.

North Sea Transition

If Smeaheia launches as planned in 2028, adding capacity to Northern Lights, Equinor will be on its way to transforming the Norwegian continental shelf into a CO2 storage network for European heavy industry and repurposing depleted reservoirs in the North Sea—an effort dubbed “Project Longship.”

Meanwhile, Germany’s Wintershall Dea (60%, operator) and TotalEnergies (40%) are exploring the Luna license area which also borders Northern Lights but is considered a separate project. All three licenses—Northern Lights, Smeaheia, and Luna—surround the Troll oil and gas field.

Fig. 1 Carbon storage license areas surround Equinor’s Troll oilfield on the Norwegian shelf.

Source: Equinor

On the same day as the Albondigas and Kinno announcement, Denmark awarded Equinor a 60% share in the country’s first CCS exploration permit, designating the Norwegian major as operator of the project to assess whether an onshore license in North and West Zealand can be developed into a safe CO2 storage facility.

Equinor is partnering with wind and solar energy developer Ørsted (owned 50% by the Danish state), and Nordsøfonden, Denmark’s subsurface resource company responsible for oil and gas production and underground CO2 storage. Each hold 20% of the license.

“Equinor expects 4–8% real base project returns for its early-phase CO2 storage business, and further value uplift potential when commercial markets are developed,” Grete Tveit, Equinor senior vice president for Low Carbon Solutions, said in a related news release. “Maturing more CO2 storage capacity aligns with our ambition of having 30 to 50 mtpa of CO2 transport and storage capacity per year by 2035.”

Drive, or Wait and Watch

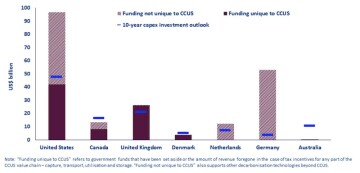

In its forecast, WoodMac analysts note that governments are largely driving CCUS projects (and those without utilization) toward final investment decisions with incentives such as those in the US Inflation Reduction Act, UK business models, Canada’s Investment Tax Credit, and the Sustainable Energy Production and Climate Transition Incentive Scheme (SDE++) in the Netherlands.

Fig. 2 CCUS government funding and 10-year investment outlook in key countries.

Source: Wood Mackenzie.

The recently announced EU Industrial Carbon Management Strategy is expected to boost further European projects, WoodMac said. The US accounts for half of the $80 billion in estimated government support already pledged for CCUS in key countries, with the UK at 33% and Canada at 10%.

The UK government is promising £20 billion ($25.5 billion) in CCS subsidies over the next 20 years, while according to the US Congressional Budget Office (CBO), US oil and gas producers are eligible for a tax credit of $85/ton of carbon dioxide they sequester, or $60/ton if the CO2 is injected for enhanced oil recovery.

In Canada, the federal government and provincial authorities in Alberta are offering multibillion-dollar tax credits to the country’s largest oil sands producers for CCS projects.

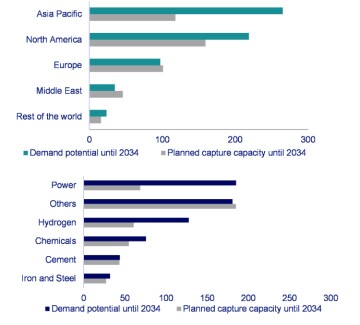

In the Middle East, Saudi Arabia and Qatar are setting targets for CCUS capacity additions in the upstream and chemicals industry, and WoodMac predicts that a third of carbon capture projects yet to be announced will come from the region.

Asia’s largest emitting countries—China and India—are holding back and will likely cause the Asia-Pacific (APAC) region to have a substantially lower capacity than what it would need under Wood Mackenzie’s base case, the report pointed out.

In July 2023, Petronas, TotalEnergies, and Mitsui & Co. formed a joint venture to make the first integrated CCS hub in Malaysia operational by 2028, with TotalEnergies bringing to the table its Norwegian experience.

“Key sectors like power and chemicals will see a large gap between demand potential and actual supply until 2034,” researchers wrote in the WoodMac report. “We expect APAC’s (deal) capture pipeline will mature through additional announcements later in the decade” if activity in Malaysia, Indonesia, and Australia to develop CO2 transport and storage hub infrastructure influences others in the region.

Fig. 3 Gap between capture demand and supply forecast.

Source: Wood Mackenzie

Balancing Costs and Benefits

Although the US leads in carbon capture with more than a third of the world’s capacity, its 15 currently operating CCS facilities only absorb 0.4% of the nation’s yearly CO2 emissions, according to the US CBO.

But even if all 121 CCS facilities currently in development in the US were to ultimately go online, the country’s CCS capacity for carbon absorption would still grow to only 3%.

This is because the cheapest industries to decarbonize—natural gas processing, ammonia, and ethanol production—account for only a small share of carbon emissions targeted for capture. Hence in the US, “the main financial incentives to use CCS are revenues from enhanced oil recovery (EOR) and a federal tax credit for capturing and storing CO2,” the CBO report explained.

ExxonMobil applied the EOR model in its 2023 acquisition of Denbury Inc., which recycles CO2 through its EOR activity and produces a low carbon crude known as “blue oil"; the supermajor has also agreed to offtake, transport, and permanently store up to 2.2 mtpa of CO2 from industrial gas company Linde’s clean hydrogen project in Beaumont, Texas, which is expected to start up in 2025.

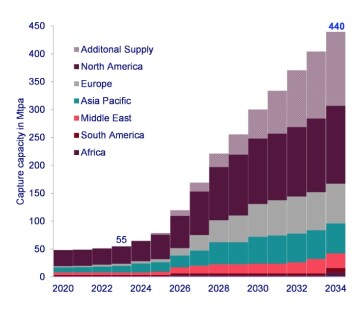

Fig. 4 Capture capacity build-out to 2034byregion.

Source: Wood Mackenzie

In March 2024, TotalEnergies announced its acquisition of Talos Low Carbon Solutions and its 25% share in the Bayou Bend CCS development, thus joining partners Chevron (operator, 50%) and Equinor (25%) in the project for industrial emitters in the Houston Ship Channel and other heavily industrialized areas on the Gulf coast of Texas.

The Bayou Bend development boasts a projected peak capacity of 30 mtpa and targets CO2 injections to start in late 2025. The project spans nearly 100,000 acres across Chambers and Jefferson counties in Texas, extending to about 40,000 acres offshore near Beaumont and Port Arthur, Texas.

With the transaction, TotalEnergies also acquired a 65% operated interest in the Harvest Bend project in Louisiana and a 50% interest in the Coastal Bend project in Texas, but the French major plans to divest itself of both after the Talos purchase closes.

TotalEnergies’ interest in Bayou Bend is tied to the project’s proximity to its Port Arthur refinery and La Porte petrochemicals facilities, which will reduce its US emissions.

In April, Houston-based energy infrastructure company Kinder Morgan agreed to lease 10,800 acres for an offshore CCS development from TGS Cedar Port Partners, a rail service operator that oversees a 15,000-acre industrial park near the Houston Ship Channel.

Gulf Coast Projects Besides injection projects, direct air capture (DAC) is also in play. In 2023, the US Department of Energy (DOE) announced up to $1.2 billion in support of developing a pair of commercial-scale DAC facilities in Texas and Louisiana capable of removing 2 mtpa of CO2.

The same year, BlackRock invested $500 million in Occidental Petroleum Corp.’s Stratos DAC facility in the Permian Basin. The project is under construction and once operational would be the largest facility of its kind in the world with a capacity of 500,000 mtpa.

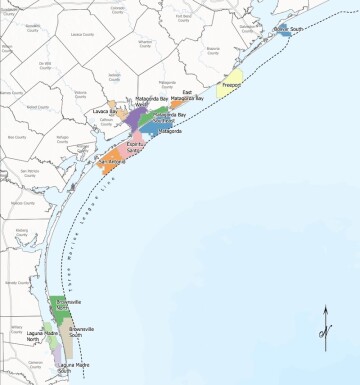

Fig. 5 Texas CCS leases up for bid.

Source: Texas General Land Office and School Land Board, RFP, 6 June 2024.

In early June of this year, the Texas General Land Office and the School Land Board put 1.13 million acres of state waters and bays along the Gulf of Mexico up for bid to develop CCS projects.

The request for proposals targets 13 zones in waters near Brownsville, Freeport, and Galveston, plus areas around Matagorda, Calhoun, and Aransas counties.

A year earlier, in August 2023, the Texas General Land Office awarded a partnership lead by Spanish oil major Repsol a contract for over 140,000 acres of pore space in two blocks—Port Aransas North and Mustang Island— owned by the state’s Permanent School Fund.

Repsol holds 40% in the project for CO2 storage off Corpus Christi, Texas, with partners Houston-based CCS project development and finance company CarbonVert (40%), Japan’s Mitsui (10%), and South Korean steel manufacturer Posco (10%).

Other blocks in the Galveston area were awarded to BP and ExxonMobil.