The wheels of the global energy mix continue to turn, making changes to the fossil fuel-dominated scenery more visible, with new pathways being forged to push decarbonization forward and accommodate emerging energy supply sectors. Regardless, the previous year still brought multiple updates on steps the oil and gas industry took to scale up the production ante.The ramp-up continues this year.

Illustration; Source: Rystad Energy

The current signs point to several factors that will have a hand in shaping the future energy sector, including further geopolitical hazards, tariff threats, and trade wars alongside multiple fuels and technologies which are expected to be available in abundance if everything goes according to plan and the energy industry continues its push to find ways to increase production from existing assets while pursuing new sources and emerging technological solutions.

Even though analysts predict lower production and demand for oil because of trade wars, oil and gas will likely remain the dominant and primary energy sources not just over the next decade but also up to 2050 and beyond unless extremely aggressive energy policy interventions encircle the globe. Is such an abrupt change in energy policy possible given the divisions and gaps in countries’ current policies and opinions on the green shift?

Given the energy security and sustainability dilemma, the oil and gas industry is shifting its primary hydrocarbon exploration focus to under-explored and unchartered offshore acreage, primarily in Asia and Africa, thus, the offshore drilling game is also moving to new frontiers to unlock more hydrocarbon resources while avoiding the hassle of ongoing litigation saga, especially in Europe and the U.S.

However, the Gulf of America, formerly the U.S. Gulf of Mexico, remains an exploration and production hotspot in the U.S. offshore arena, and so does Norway within the European waters. While energy security concerns turn the oil, gas, and liquefied natural gas (LNG) plots into fertile ground for investment in the global energy landscape, not all regions are ripe for such plays.

This is due to other challenges, such as high inflation, emerging tariff wars, geopolitical upheavals, supply chain constraints, elevated costs, shifting investor sentiments, and climate change woes, which hold the potential to prompt new market challenges to arise. Which offshore energy playgrounds present the best opportunity for investors to get a bang for their buck?

In a bid to find an answer to this puzzle, Offshore Energy conducted a poll on a small sample of 100+ voters involved in the energy arena, asking them to pick the right answer to the question: Which of the countries/regions holds the reins of the oil, gas, and/or LNG sector’s growth with the highest level of investor confidence? The majority of participants or 41%, selected the United States of America, followed by 29% who opted for the Middle East, then came 17% who gave their votes to Norway, 9% who saw Africa as the best investment landscape, and 4% who voted for Asia brought up the rear.

Given the prevailing sentiments in these regions, especially the U.S., which is experiencing an oil and gas boom in terms of encouraging government policy, these results, despite collecting the views of only a small ripple in the ocean of energy professionals, do seem to match the current overall energy industry fundamentals on the global oil and gas scene.

This content is available after accepting the cookies.

A recent Global Witness analysis underlined that Big Oil’s historic liability tops $1 trillion, thus, it concluded that a climate tax to cover a decade of Loss and Damage could be raised from the world’s biggest oil and gas companies for their alleged historic liability in polluting the planet. Others argue that such a move would put the security of supply at risk and increase prices.

While some, like the International Energy Agency (IEA), claim that geopolitical upheavals are bringing home the need for faster expansion of clean energy, others are convinced these challenges reinforce the necessity of clinging to proven technologies and sources of supply, such as oil and gas alongside LNG, which have earned their stripes and shown they can keep the lights on regardless of the whims of the weather while exploring new energy options.

In line with this, Mike Sommers, American Petroleum Institute’s President and CEO, who highlighted the need to secure America’s energy advantage through domestic resources rather than relying on other regions at a time of rising worldwide geopolitical volatility, at the end of last year called for policies that ensure the U.S. could meet “energy needs tomorrow, not just today.”

Opponents of fossil fuels cite New InfluenceMap research and similar works to raise the alarm over the oil and gas industry’s alleged playbook of narratives and arguments that contradict so-called science-aligned policy, which is employed to “systematically oppose, weaken, and delay” the energy transition since at least 1967 as part of their advocacy repertoire against renewable energy and other clean and low-emission alternatives that threaten to undermine their position.

Based on the IEA’s findings, the natural gas demand is rising at a stronger rate this year than in the previous two due to the turmoil of the global energy crisis but new gas supplies coming to market in 2024 remained limited as a result of the relatively slow growth of LNG production while geopolitical tensions fuel price volatility.

Keisuke Sadamori, IEA’s Director of Energy Markets and Security, commented: “The growth we’re seeing in global gas demand this year and next reflects the gradual recovery from a global energy crisis that hit markets hard. But the balance between demand and supply trends is fragile, with clear risks of future volatility. Producers and consumers must work together closely to navigate these uncertain times while taking into account the need to advance clean energy transitions to ensure a secure and sustainable future.”

A report from the International Energy Agency predicted that global growth of renewables up to the end of the decade is set to match the entire current power capacity of major economies, paving the way for the world to come closer to its goal of tripling renewables. This aligns with the IEA’s ‘World Energy Outlook 2024,’ which pinpointed critical choices facing governments and consumers as a time of “more ample supplies nears and surging electricity demand reshapes energy security.”

The report delved into fragilities in the current global energy system, such as geopolitical strains and regional conflicts, which are said to lay bare the necessity for “stronger policies and greater investments to accelerate and expand the transition to cleaner and more secure technologies.”

This content is available after accepting the cookies.

Fatih Birol, IEA Executive Director, remarked: “In the second half of this decade, the prospect of more ample – or even surplus – supplies of oil and natural gas, depending on how geopolitical tensions evolve, would move us into a very different energy world from the one we have experienced in recent years during the global energy crisis. It implies downward pressure on prices, providing some relief for consumers that have been hit hard by price spikes.

“The breathing space from fuel price pressures can provide policymakers with room to focus on stepping up investments in clean energy transitions and removing inefficient fossil fuel subsidies. This means government policies and consumer choices will have huge consequences for the future of the energy sector and for tackling climate change.”

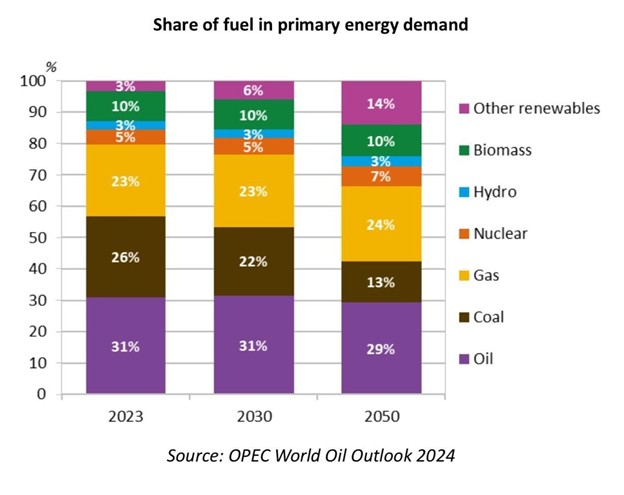

On the other hand, OPEC’s ‘World Oil Outlook (WOO)’ from September 2024 underscored the domination of fossil fuels in the global sphere of energy supply up to 2030, when they are expected to represent 77% of the energy mix. The cartel claims that the IEA’s ‘World Energy Outlook (WEO),’ which projects a 75% share for fossil fuels in 2030, a spike from the 73% share previously reported in the WEO 2023, confirms its projections of higher fossil fuel use.

The International Energy Agency has confirmed the expected shift in energy markets in the coming years. While highlighting that the world could see relatively ample supplies of key fuels and technologies, the IEA also warned about geopolitical risks that are expected to remain. Therefore, the IEA is adamant in its belief that governments and consumers’ reactions would have major consequences for energy and climate developments.

The net-zero zest’s intensity switches gears with each election and political change, thus, drastic rewriting of the global energy mix is not likely to be on the cards with the current political leaders on the stage, especially not as the world is grappling with geopolitical implications of a potential escalation in the already conflict-ridden Middle East, the treat of a new world order being forged as the fabric of the existing one continues to be eroded.

Eni outlines in its global energy statistical review that fossil fuels managed to meet four-fifths of demand last year, with an approximate growth rate of 2%, accounting for around 80% of energy demand. The Italian giant’s data shows that oil made up 30%, coal 28%, and gas 23% of the energy mix, despite the rise in the share of solar PV and wind, which was below 3%.

While the necessity of bringing down the greenhouse gas (GHG) emissions footprint is undeniable, the expected rise in population growth and increasing energy demand are laying bare the need for enduring investment in all energy sources, including oil and natural gas, to avoid supply shortages and price shocks down the road. Many are convinced the worldwide energy mix cannot survive the trials and tribulations of the future if oil and gas taps are turned off tomorrow.

The rising emphasis on worldwide energy security puts hydrocarbons firmly at the forefront of further progress and security of supply, even though renewables are destined to continue to take up more and more space in the energy mix. Every era has its ups and downs, but energy experts continue to call for further investment in all sources of supply while highlighting the crucial place oil and gas will continue to play even beyond 2050, as the world works to diversify the energy mix and ensure enough supplies to meet the spike in demand.

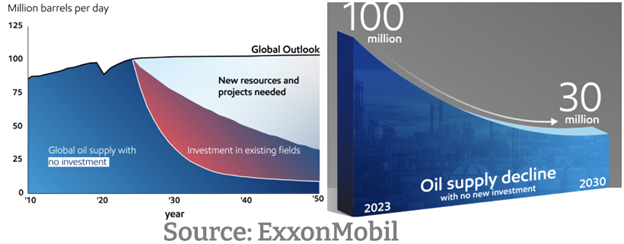

This, in turn, pinpoints a further uptick in oil and gas as a legitimate goal for the sake of global energy security, given the declining rate of worldwide production from existing assets. Those like ExxonMobil are convinced that the security of supply puts the investment in more oil, gas, and LNG on solid enough ground to withstand the test of time.

“The world would experience severe energy shortages and disruption to daily lives within a year of investment ceasing. Given price responses to past oil supply shocks, the permanent loss of 15% of oil supply per year could raise oil prices by more than 400%. By comparison, prices rose 200% during the oil price shocks of the 1970s. Within 10 years, unemployment rates would likely reach 30%. That’s higher than during the Great Depression of the 1930s,” outlined the U.S. oil major in its view of energy demand and supply through 2050.

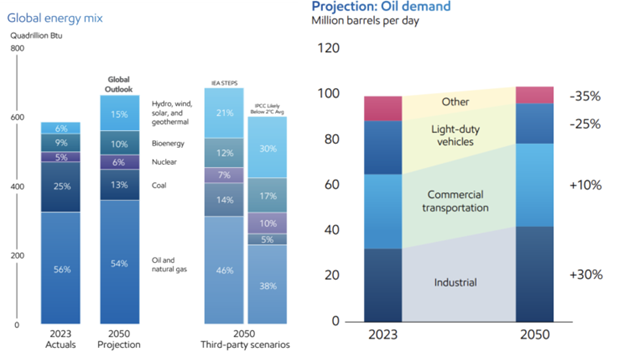

While spotlighting the need for investment in new technologies, ExxonMobil also forecasts a fourfold boost in wind and solar power within the energy mix by 2050, however, the company warns that any energy policy to keep oil and gas in the ground would not be just, as these sources are predicted to make up 50% of the energy mix in 2050 with a plateau in oil demand beyond 2030, keeping it steady at above 100 million barrels per day through 2050.

While noting that renewables alongside oil and gas will be key to meeting the estimated 15% surge in energy demand by 2050, the U.S. firm underscored: “Yes, changes in the world’s overall energy mix are coming. But the Global Outlook and various third-party scenarios are clear – oil and natural gas will remain essential.”

Courtesy of ExxonMobil

Therefore, if the world is serious about finding ways to be on top of energy demand and pursue affordability by upholding reliability, lower costs, and infrastructure benefits of the current energy system while innovating and upscaling it further as new technologies become available, ExxonMobil’s outlook points out that certain technologies and solutions need to be leveled up to keep up the energy demand pace as population goes from 8 billion to nearly 10 billion in 2050.

These entail further inroads in energy efficiency, additional uptick in renewables, and lower-emission technologies, such as carbon capture and storage, hydrogen, and biofuels, to reach a low-carbon and carbon-free future on today’s wishlist. The U.S. player calls for policies that enable a level playing field for all technologies to compete “without fear or favor” with governments offering incentives if no market exists and initial costs are deemed too high.

Such action is seen as a way to get the ball rolling in the right direction. However, once these take off, the firm believes such incentives should be discontinued over time as the private sector picks up the torch while markets develop to reach net-zero aspirations and curb emissions. Even though ExxonMobil sees “enormous progress” so far, the work is not done yet, thus, it concludes that more remains to be undertaken.

During the quest to decarbonize the energy mix and usher in a more sustainable future, the U.S. energy giant underlines the need to keep several aspects firmly in mind. These refer to all energy types having their place in the mix, renewables continuing to have the fastest growth spurt, coal set to decline the most, oil and gas being seen as ‘essential’ elements under any credible scenario, and lower-carbon technology still requiring government policy support to up its ante but ultimately the baton must be passed on to market forces.

The energy outlook was summed up succinctly by Darren Woods, ExxonMobil’s Chairman and CEO, who laid down the law by saying: “To get serious, three things are needed: supportive public policy, significant technology advancements, and a smooth transition from government subsidies to market-based mechanisms.”

Based on Global Data’s report, 237 LNG projects were on the list to start operations from 2024 to 2028, out of which 154 represent regasification projects, and 83 are liquefaction projects. While Asia dominates globally with the highest number of LNG regasification projects (99) by 2028, China leads among the countries with 35 regasification projects expected to start operations by 2028. Regarding liquefaction projects, North America spearheads the growth, with the U.S. accounting for 26 projects.

Decom costs and cyber threats on the rise

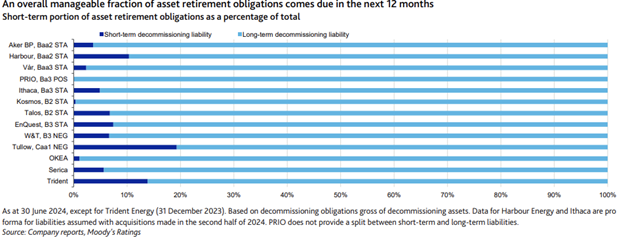

Meanwhile, Moody’s research indicated last year that oil and gas companies with downstream operations in Europe would likely report significantly lower earnings from these over the following 12-18 months, with Preem Holding, Neste, CEPSA, MOL Hungarian Oil and Gas, and ORLEN anticipated to be among the most exposed while the impact for Shell, TotalEnergies, BP, Eni, Repsol, and OMV were expected to be more balanced.

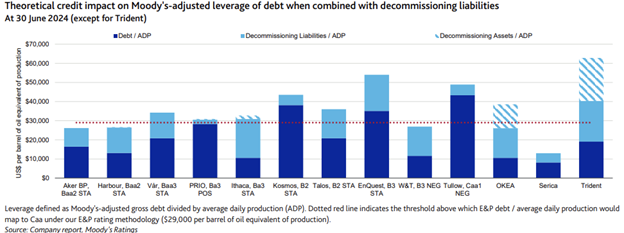

The research also shows that decommissioning costs of mature oil and gas assets have an increasing influence on credit quality for smaller E&P companies in mature offshore basins, thus, this is set to become a significant risk in less favorable market conditions, as the aggregate decommissioning liability for the analyzed companies is $22.4 billion, representing more than 50% of total liabilities for some operators in mature basins.

Since the estimated annual decommissioning costs keep rising, the indicators last year pointed out that they would total £2.4 billion a year on average to 2032 in the UK’s North Sea. While carbon capture and storage could delay decommissioning costs and diversify business profiles, Moody’s findings show this is unlikely to neutralize carbon transition risk exposure.