Is the US Shale Sector Expecting a Happy New Year?

A recent wave of megadeals is weighing on the mind of many oil and gas executives in Texas, New Mexico, and Louisiana.

Oil prices have comfortably remained above $70/bbl for most of this year, yet the upstream sector in and around Texas is feeling a bit uneasy.

Oil and gas executives shared their concerns about the business as they head into the new year in a recent survey by the Dallas branch of the US Federal Reserve Bank.

This survey, covering exploration and production and service companies based in Texas, southern New Mexico, and northern Louisiana, noted that while oilfield activity was almost unchanged from the prior survey, oil output growth is slowing and equipment utilization is declining.

The Dallas Fed’s quarterly survey indicated mounting pessimism among oil and gas producers, as reflected in its outlook index which plummeted from 46.8 points to -9.0. The uncertainty index also rose, from 39 points to 46.1, again reflecting a souring mood.

That said, when more than 140 executives from both producers and service companies were asked about next year’s spending plans, only 13% said they planned to “decrease significantly.” Another 18% said they would “decrease slightly.”

The most common answer, at 33%, was “increase slightly,” while the remaining 10% plan to “increase significantly” their capital programs next year.

Drivers behind the worsening sentiments, as listed by exploration and production (E&P) executives, include investor hesitance to finance new projects, higher prices for goods and services, and US government energy and environmental policy.

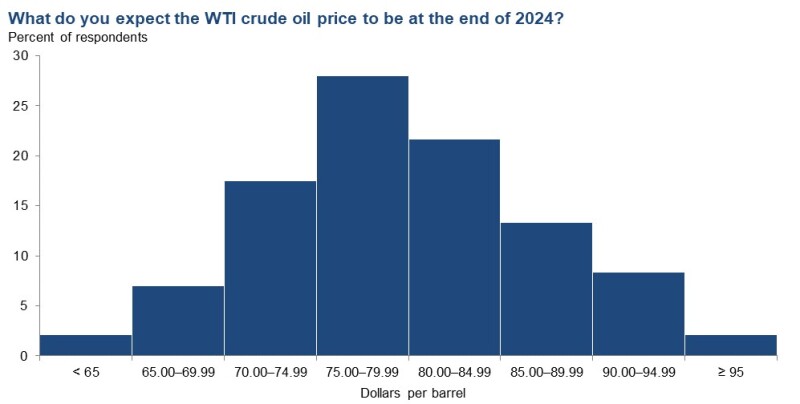

They are also wary of a softening market for US crude, which has seen prices dip 20% from September’s high-water mark of $91/bbl. Notably, the overwhelming majority of those who took the survey are budgeting next year based on prices at or above $70/bbl with a significant share expecting prices to end the year above $80/bbl.

However, if crude falls below the $70/bbl handle due to oversupply, this would likely depress Permian activity and curtail spending next year—which some survey takers said might lead to a sudden spike in oil prices as the supply/demand pendulum swings back.

Others placed the responsibility for an improvement in prices squarely on the shoulders of international exporters.

“The big question is will OPEC+ be able to keep the price of crude oil up,” commented one of the respondents.

“OPEC's failure to secure binding oil production cuts by certain members is a concern,” said another survey respondent, who posited that Saudi Arabia might take matters into its own hands and “flood the market with crude to punish nonconforming OPEC members and US producers, similar to the events of 2014.”

Executives from 143 oil and gas companies in Texas, New Mexico, and Louisiana answered this question between 6-14 December, 2023. The average response was $78/bbl while during the survey period US oil prices were nearly $70/bbl.

Source: Federal Reserve Bank of Dallas.

Concerns Over Consolidation

Impossible to miss in the survey responses from service companies are the concerns expressed over the recent wave of mergers and acquisitions among their E&P customers.

Though the latter deal did not impact the Permian Basin much—Hess’ assets are focused on North Dakota’s Bakken Shale and offshore Guyana. Both transactions signaled that the runway for many US independents is running out.

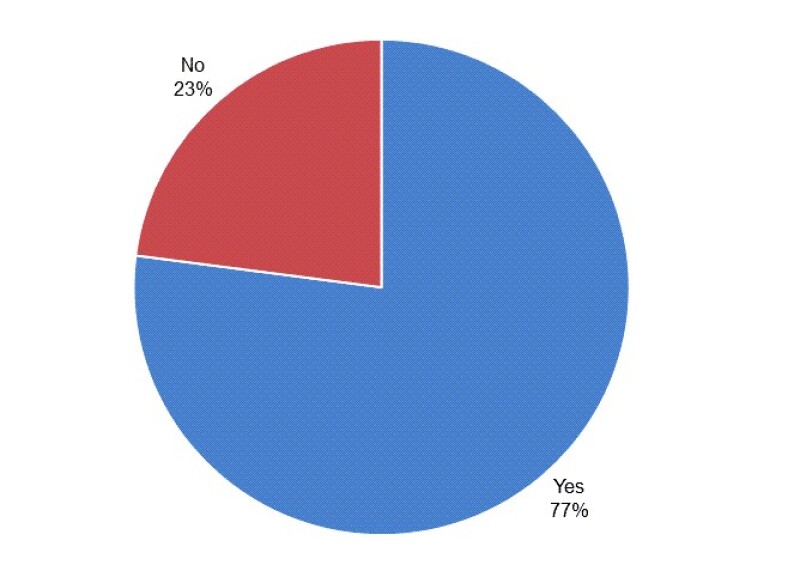

The Dallas Fed survey asked whether executives saw more megadeals like these in store over the next 2 years. A stout 77% answered in the affirmative.

One executive from an oil and gas company took issue with the fact that the $175 billion in US upstream merger and acquisition deals made this year exceeds the combined value of all the deals made in the previous 3 years.

“Majors are explicitly investing on the thesis that the back end of the forward curve for oil is just plain wrong. Whatever Excel model they are using to justify these prices isn't going to align with their consolidate-and-cut operations,” they said, adding, “Inventory for US onshore will be extremely valuable in 5 years as shale inches toward death and moves to terminal decline. Prices are likely closer to $150 than $50 at the end of the decade.”

The complaints from service providers are more existential in nature, as shale sector megadeals directly translate to business attrition. Most buyers waste little time stacking the sellers' rigs and trimming their supplier and vendor lists in order to realize some immediate savings.

Some service provider executives described the shrinking number of operators in the shale sector as “a negative for the industry” and “not helpful.”

“The consolidation of operators will impede the growth and sustainability of the oilfield service sector. This will lead to the demise of small independent oil and gas operators, as they will be unable to obtain reasonable pricing from the few remaining service providers,” said one service firm executive.

The respondent also suggested that the US federal government should step in and “stop the wholesale purchases of these large companies as it is detrimental to the energy health of the nation and economic stability to our communities.”

Another oilfield services executive considers consolidation to be inevitable now that buying reserves has become more affordable than finding new volumes.

“With the significant number of privately held operators looking for exits and value expectations balancing between buyer and seller, we should expect more public companies buying the privates to continue,” they said.

Of the 122 executives who responded, 77% expect more acquisitions of $50 billion or more to occur in the next 2 years while the remaining 23% do not.

Source: Federal Reserve Bank of Dallas.

Too Small To Mitigate

When the Dallas Fed survey asked the executives about their firm’s environmental plans next year, the answers largely depended on whether the respondent represented a large or small producer.

Just over half of the 19 respondents from large producers, considered those with volumes above 10,000 B/D, said they will focus on reducing CO2 emissions, while two-thirds said they will reduce methane emissions, which are considered to be the more potent greenhouse gas.

Additionally, almost 80% said they would be attempting to lower their flared-gas volumes over the next year.

But for those oil and gas companies with a production profile below 10,000 B/D, of which 67 took part in this part of the survey, there is much less enthusiasm to tackle such issues.

Only 22% of small E&Ps said they would be lowering CO2 emissions next year while a third said they planned to reduce methane emissions. Only 18% had plans to reduce flaring.

When it comes to having any mitigation plans at all, 11% of large producers acknowledged they had no plans compared with 51% of the smaller producers.