New IEA Report: "Next-Generation" Geothermal Can Go Global, But Oil and Gas Industry Must Show the Way

The upstream sector could help unlock geothermal energy’s potential to drive $1 trillion in project spending over the next decade.

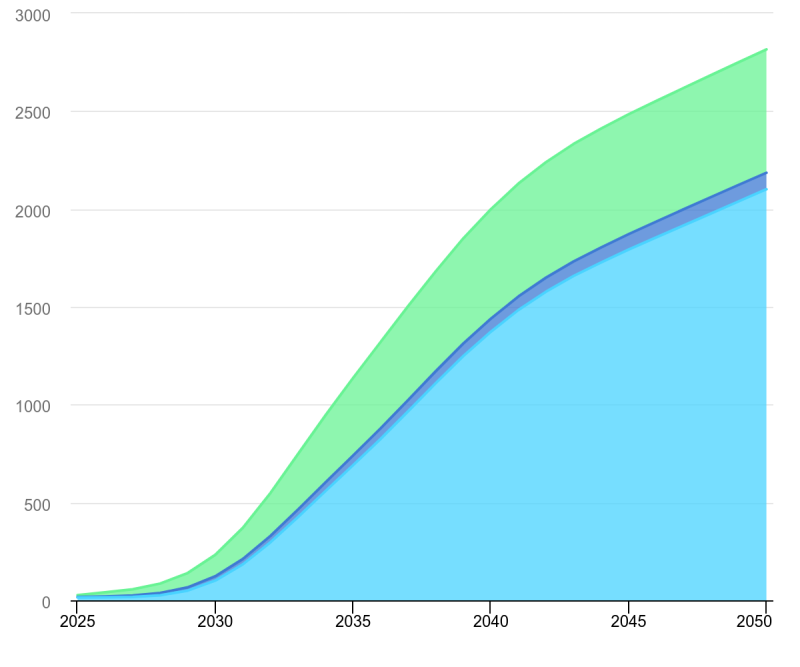

The IEA estimates that $1 trillion in spending will be needed by 2035, with the figure nearly tripling to $2.8 trillion by 2050.

Source: Getty Images.

Geothermal energy could meet 15% of global electricity demand growth by 2050, if significant cost reductions are achieved, according to a new report from the International Energy Agency (IEA).

Such an expansion would boost geothermal’s share of the global energy mix from its current 1% to 8%—an increase equal to the combined electricity demand of the US and India today.

This scenario hinges on what the IEA calls “next-generation geothermal technologies” achieving their full market potential in rapid fashion. The technology category includes the recently emerged closed-loop geothermal systems along with enhanced geothermal systems (EGS) that rely on horizontal drilling and hydraulic fracturing techniques.

In comparison to the 15% demand growth the IEA is projecting to be possible for these new technologies, it sees only 1% demand growth for traditional geothermal energy.

For next-generation geothermal to reach the trajectory outlined by the IEA, it will require a massive capital investment—a development that could translate into a windfall for the upstream industry.

The IEA estimates that $1 trillion in spending will be needed by 2035, with the figure nearly tripling to $2.8 trillion by 2050. About 75% of the total investment would go toward wells for electricity generation, while the remainder would fund heat production for residential and industrial use.

The oil and gas industry has yet to embrace geothermal energy as enthusiastically as other clean-energy investments, but the scale of the opportunity could shift attitudes. The IEA noted that the upstream sector stands to benefit both as a supplier and as an active participant, given it already holds about 80% of the components required to complete a geothermal project.

“The industry has transferable skills, data, technologies, and supply chains that make it central to the prospects for next-generation geothermal,” the report said. It also noted that by adding geothermal to their portfolios, upstream companies can hedge against projected declines in oil demand, which some, including the IEA, foresee emerging as early as the end of the decade.

The estimated cumulative investment for next-generation geothermal between 2025 and 2050.

Source: International Energy Agency.

Where Geothermal Will Go Big

The IEA said its new report, produced in partnership with Project InnerSpace, marks the first-ever country-level assessment of geothermal potential.

China, the US, and India stand out as the most likely adopters of new geothermal systems, collectively accounting for about 75% of the world’s new capacity over the report’s timeline.

China could lead the way by contributing roughly 40% of global geothermal capacity additions by 2050. The country requires around 700 GW of low-emission, dispatchable power capacity over the next 25 years, with the IEA estimating that next-generation geothermal systems could supply about half of that figure.

The US follows China in the IEA scenario thanks to its incumbent role in developing much of the technology around EGS which stemmed from innovations in the US-based unconventional oil and gas sector. With policies supporting geothermal already in place, the IEA foresees geothermal displacing bioenergy use in the US before competing with new nuclear, solar, and wind power projects.

India becomes the third-largest adopter of next-generation geothermal where it displaces solar power installations along with coal-fired power plants.

Major Cost Reductions Possible, and Needed

The IEA cautions that achieving its vision for next-generation geothermal energy rests on the nascent sector’s ability to rein in costs—an effort that will likely require substantial involvement from the oil and gas industry.

But by becoming intertwined with the upstream sector and leveraging its deep technological expertise and project management capabilities, the IEA estimates conventional geothermal costs could be halved, while next-generation geothermal costs could decline by as much as 80%.

This would bring EGS costs to around $50/MWh, making geothermal a cheaper option than other low-emission power sources, such as hydroelectric and nuclear, and competitive with solar and wind farms.

The report highlights several areas where oil and gas expertise could aid in achieving these cost reductions. For example, persistent challenges with data quality, accuracy, and the aggregation of public geological surveys remain significant hurdles. The IEA noted that closer collaboration with the oil and gas sector could “drastically improve data coverage and quality.”

That said, drilling, which accounts for 60 to 80% of total geothermal project costs—including power plants and transmission infrastructure—is the key target for cost reductions.

Today, EGS projects, such as those developed by Houston-based Fervo Energy and Utah’s FORGE initiative, are seen as the most technically ready for large-scale deployment.

The IEA estimates that the first-of-their-kind EGS projects in the US cost nearly $14,000/kW, which is about twice the cost of nuclear power, and thus far too high for widespread adoption.

However, the agency projects that with supportive policies, increased investment, and significant involvement from the oil and gas industry, costs could drop to $3,000 to $7,000/kW by 2035 and $2,000 to $5,000/kW by 2050.

The IEA said this would result in a 300-MW EGS project dropping from $4 billion to between $2 and $1 billion by 2035. The capex by 2050 for the same size project falls to between $1.2 billion on the high side and just $600 million on the most optimistic end of the spectrum.

Casting Doubt on Oil Well Conversions

There is one area where the overlap may not be as significant as once believed.

The concept of converting abandoned oil and gas wellbores into geothermal wells has been considered in recent years as a potentially cost-effective solution and has even undergone limited field testing.

However, the IEA and Project InnerSpace report raises questions about the scalability of the approach compared with purpose-built geothermal wells.

Even if an existing asset can meet heat and flow rate requirements, ensuring a high degree of wellbore integrity must also be established—a characteristic not often associated with older wells.

As the IEA report adds, older wells “may be subject to lifetime durability challenges under new flow regimes and chemistries, in addition to corrosion, erosion, and scaling problems.”

The high workover costs associated with older wells could further undercut the economic appeal of conversions, the report adds, and flexible permitting frameworks would be necessary to support such projects.

Another problem is that abandonment rules for oil and gas wells remain in place even if a well is repurposed for geothermal use. This creates a notable liability for developers, as wells would still need to plan for costly plug and abandonment operations to prevent methane leaks and comply with local regulatory standards.

The full report can be downloaded from the IEA's website here.