BP Takes Majority JV Stake in Wind Project Offshore Korea

BP’s deal with Norway-based Deep Wind Offshore aims to generate nearly half of the 13 GW of electricity Korea plans to produce from offshore wind by 2030.

BP has formed a joint venture with Deep Wind Offshore, a Norwegian developer and owner of offshore wind projects in Europe and Asia Pacific, acquiring a 55% stake in an early-stage offshore wind portfolio with the potential to generate 6 GW of electricity from four projects in South Korea.

The deal, inked on 14 February, came a week after media had criticized BP for appearing to scale back its carbon emissions goals while it joined fellow majors in reporting a more than twofold increase in 2022 profits year on year.

BP’s record $27.7 billion windfall was due to the war in Ukraine which kept oil prices above $100/bbl for a significant part of the year. As markets tightened and supply chains realigned globally, fossil fuel sales drove profits to record levels among the supermajors: ExxonMobil, $55.7 billion; Shell, $39.87 billion—its highest profit in over 100 years; Chevron, $36.5 billion, TotalEnergies, $36.2 billion. Eni will report on 23 February.

In announcing BP’s yearend results on 6 February, CEO Bernard Looney said his company now aims for a 20-30% reduction in carbon emissions from oil and gas production by 2030, an apparent backslide from BP’s earlier stated goal of 35-40%, though Looney said BP is still on track to meet its 2050 objectives.

Looney’s further comments that BP would also cut back less on oil and gas production this decade to the extent it had previously thought possible, however, created a stir with some media suggesting that BP will deemphasize less profitable renewable energy. Not true, according to BP.

Capital Investment Is Abundant in Today’s Parallel Universes

BP is on track to increase capital spending on its low-carbon businesses by $8 billion over the next 8 years, a commitment that Anja-Isabel Dotzenrath, BP’s executive vice-president for gas and low-carbon energy, told the Financial Times, proves the company does not plan to waiver from its goal of generating 50 GW of renewable power by 2030.

That is $1 billion per year is in addition to the $7-9 billion already allocated annually to low-carbon initiatives, a cumulative $55-65 billion over 2023-2030, divided between BP’s existing bioenergy, convenience and EV charging businesses, and the company’s developing hydrogen, renewables and power businesses, BP said in a news release detailing its strategy.

There is “absolutely no link between confidence in returns from renewables and the production target on the oil and gas side,” Dotzenrath said in the FT interview published on 13 February in the midst of the media-fed controversy. “I have the support to deploy $30 billion of capex to the end of the decade in my business...and I’ve seen what this company is capable of doing.”

Now Hiring: BP To Double Wind Power Engineering Staff

The next day, BP inked its Korean offshore wind venture with Deep Wind, and the day after that, Matthias Bausenwein, BP’s head of offshore wind, told Reuters his division will hire over 100 new employees in coming months as it builds towards doubling its current team of 800 over the next 2 years. The objective is to build an “engineering backbone” for BP’s offshore wind activity in Europe, Bausenwein said.

Since Looney became CEO 3 years ago, BP has shifted its hiring focus from traditional oil and gas jobs to those supporting growth of low-carbon businesses. Last year, BP recruited Bausenwein fromØrsted, the Danish power company which 30 years ago built the world’s first offshore wind farm; along with his boss, Anja-Isabel Dotzenrath, who previously headed Germany’s RWE Renewables.

In terms of profitability, offshore wind has lagged other low-carbon options. BP reported that it expects returns to exceed 15% from its bioenergy, convenience and EV charging businesses combined. It expects unspecified but certainly double digit returns from hydrogen, but only a 6-8% return from renewables.

Given the profits currently on the table, BP is targeting “short-cycle fast-payback opportunities” in oil and gas with $8 billion in additional investment between now and the end of the decade while at the same time investing another $8 billion in what Looney called “energy transition growth engines."

BP also plans to increase its dividend by 10% and add $2.75 billion in stock buybacks.

“To tackle that, action is needed to accelerate the transition,” Looney said at BP’s yearend analysts call earlier in February. “And—at the same time—action is needed to make sure that the transition is orderly, so that affordable energy keeps flowing where it’s needed today.”

Hence, among other vectors, BP has of late accelerated its expansion into offshore wind, forming joint ventures in the UK, Germany, the US, Japan and now South Korea in a move that may prove providential as business models and technologies mature.

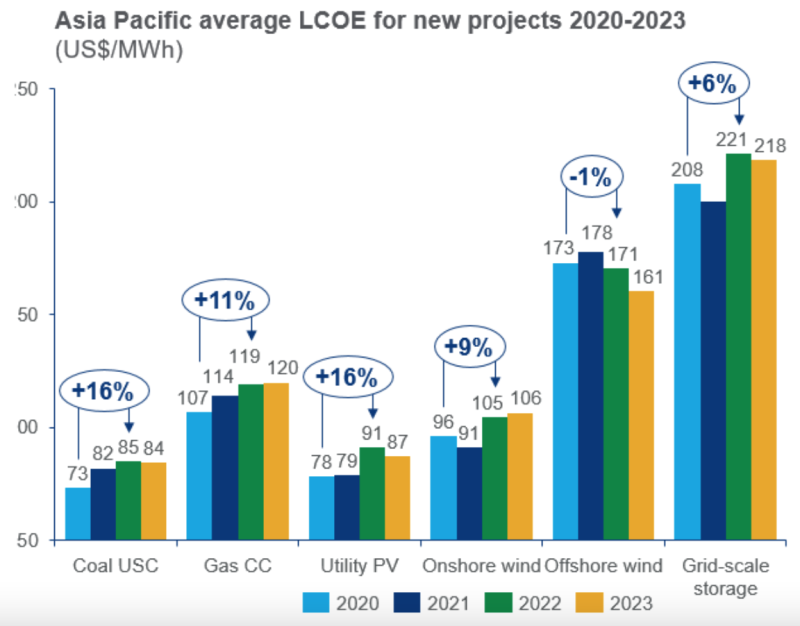

Answers May Be 'Blowing In The Wind' in AsiaPac

In Asia Pacific (AsiaPac), levelized costs of electricity (LCOE) for utility solar and onshore wind have risen 16% and 12% respectively since 2020, driven by rising costs of equipment, construction, and interest rates. That trend though is expected to reverse in 2023—particularly regarding offshore wind, Wood Mackenzie argues in a news release promoting its latest overview of the competitiveness of power and renewables in AsiaPac.

While the LCOE for onshore wind is expected to rise slightly this year, offshore wind is slated to experience the greatest decline in costs of producing electricity when compared with other power generation alternatives including coal and gas, WoodMac found, with costs trending downward across countries throughout the region.

In Asia Pacific, new offshore wind project could see the biggest drop in LCOE in 2023 when compared to other energy projects.

Source: Wood Mackenzie Asia Pacific Power Service.

So far as offshore wind is concerned, BP entered AsiaPac in earnest in March when BP Alternative Energy Investments Ltd. took a 51% stake in a JV with Marubeni Corporation to develop offshore opportunities in Japan where the two companies will also explore opportunities for hydrogen, according to Marubeni.

Marubeni was one of the first developers involved in the the Fukushima Floating Offshore Wind Farm demonstration project; it also participated in the offshore wind farm project at Akita Port and Noshiro Port—the first large-scale commercial based offshore wind project in Japan, the integrated trading and investment conglomerate reported in a news release at the time of the signing with BP.

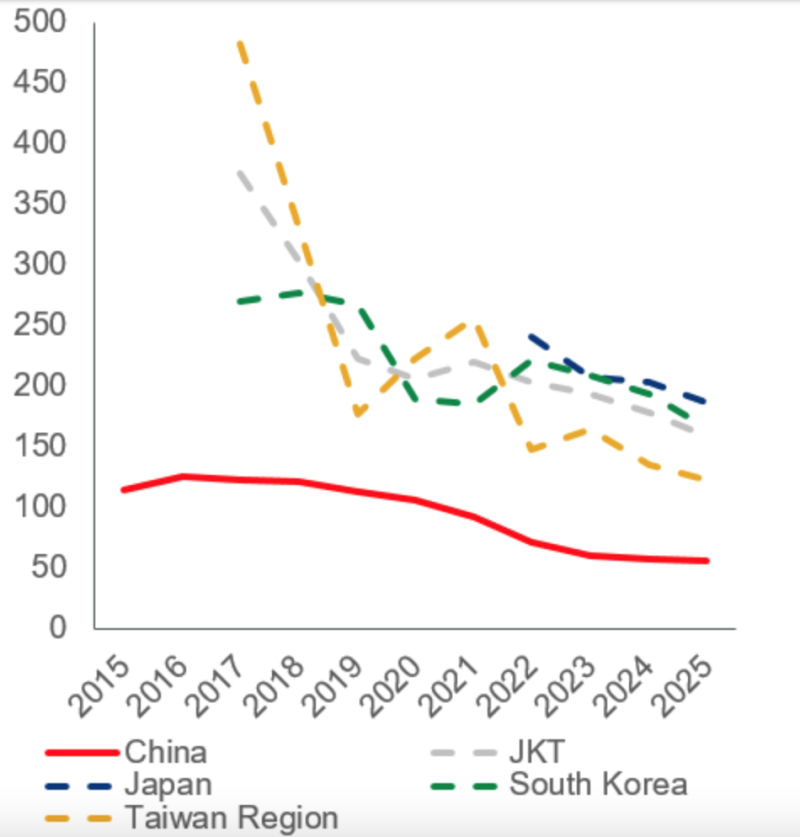

Chart showing the average offshore wind levelized cost of electricity in $/Mwh reveals how across AsiaPac, costs of new offshore wind projects are dropping.

Source: Wood Mackenzie’s Asia Pacific Power Service.

With stakes in 21 power projects globally, Marubeni and its partners also secured seabed leasing rights for the ScotWind project in Scotland, UK in January 2022, which has a maximum capacity of 2,600 MW.

Similarly in Korea, BP’s new partner, Deep Wind Offshore, has secured site exclusivity for the first two of four offshore wind projects it envisions in South Korea which aims to source 22% of its energy from renewables by 2030.

Norway’s Deep Wind has signed a memorandum of understanding (MOU) with Korea’s state-owned power generation company, East West Power (EWP), to collaborate on four projects that would exceed 4GW of floating and bottom fixed offshore wind in South Korea, according to Deep Wind’s website. EWP currently accounts for 11.2 GW of all power generation facilities in South Korea.

An international developer and owner of offshore wind projects, Deep Wind has been active in Korea since 2006 through its owner, Knutsen Group which is currently one of the biggest clients to the Korean shipbuilding yards. BP itself boasts a 40-year presence in the country through its oil and LNG trading activities and its Castrol lubricants business.

The permitting process began following installation of wind measurement devices in 2021 and 2022 and now BP and Deep Wind Offshore will together install additional wind measurement systems and secure electricity business licenses, according to BP.

In Norway, Deep Wind Offshore is developing Utsira Nord and Sørlige Nordsjø II together with EDF Renewables. The company is backed by industrial owners Knutsen Group, Haugaland Kraft and SKL from the shipping/offshore and utility sectors.

Offshore Wind, New Territory But Not BP’s First Rodeo

In terms of onshore wind, BP brings to the table its US experience as operator of an onshore wind portfolio with a generating capacity of 1.7GW. In the offshore wind segment, BP is developing together with Norway’s Equinor, the Empire Wind and Beacon Wind projects off the East Coast which have the potential to generate up to 4.4GW.

BP is also building its global offshore wind presence with a 5.2 GW net capacity pipeline and, in the UK, it is developing the Morgan and Mona projects in the Irish Sea, and the Morven project in the North Sea off Scotland with German utility, EnBW, as its partner. Together, the projects have potential gross generating capacity of around 6 GW.